While the debate proceeds over some details of the American Health Care Act, it’s worth pausing to take another look at how awfully misnamed the so-called “Affordable” Care Act has turned out to be, especially for people who buy their health plans on their own, rather than obtain it through an employer. While advocates and politicians have cited numerous examples of people facing huge premium increases, ACA advocates have been able to respond that those are cherry-picked cases, or that premiums were increasing before the ACA and would have increased anyway.

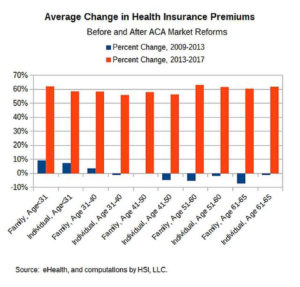

Those responses are no longer plausible. It turns out that across the board, for all ages and family sizes, for HMO, PPO, and POS plans, premium increases averaged about 60 percent from 2013, the last year before ACA reforms took effect, to 2017. In same length of time preceding that, all groups experienced premium increases of less than 10 percent, and most age groups actually experienced premium decreases, on average.

These findings come from new data from eHealth, which not only sells ACA Marketplace health plans, but sold a wide variety of health plans through its own website for many years before the ACA was passed, as well as both on and off the Exchanges after the ACA took effect. For years starting with 2014, the data include ACA-compliant, non-employer-sponsored plans sold both on and off exchanges. It does not include premium subsidies, which in any case are available only to on-exchange purchasers with qualifying income.

The data allow us to break down the pre- and post-ACA changes by age, individual vs. family, and plan type. Overall, Health Maintenance Organization (HMO) premiums actually decreased 4.6% in the four years before the ACA reforms came into effect (that is, from 2009 to 2013), but increased 46.4% in the first four years under the ACA. Point-of-Service (POS) premiums decreased 14.9% before the ACA, and increased a whopping 66.2% afterwards. Premiums for the more common Preferred Provider Organization (PPO) plans increased 15% in the four years before the ACA, and 66.2% afterwards.

Percentage change in average premiums across plan types (HMO, POS, PPO) before and after implementation of ACA market reforms on Jan. 1, 2014. Data from eHealth.com, computations by HSI, LLC.

In each case, the increases differed among age groups, with families headed by those under 30 and over 50 generally being hit the hardest by the ACA premiums increases. However, once we remove the self-sorting into different plan types, and average each age group and household type (i.e., family or individual), the results are very consistent – in the four years before the ACA, every age group and family type either experienced a premium decrease, or an increase of 9.2% or less. However, in the first four years of the ACA, every age group and household type experienced an increase of between 56.0% and 63.2%. For something as complex as health care, that’s a pretty narrow range. The dollar amounts of the increase varied from $2,524 for an individual between the ages of 31 and 40, to $12,040 for a family headed by someone over age 60. But the percentages are remarkably consistent: The ACA raised premiums by about 60 percent.

The only plans that didn’t fit this pattern were the previously-rare EPOs – “Exclusive Provider Network” plans, which have restricted, generally small, networks of providers, and provide absolutely no out-of-network coverage, except possibly for emergency care. Their premiums increased 18.6% in the four years before the ACA, and 15.9% in the four years afterwards. These highly undesirable plans were rarely purchased in the pre-ACA era, but have become much more widespread since 2014, as more patients found themselves priced out of more traditional plans because of ACA reforms, and more insurance companies offered “narrow network” EPO plans as a way of satisfying regulators demanding “reasonable” premiums.

One of the many problems with EPO plans is that procedures often require several providers – say, a hospital, a surgeon, an anesthesiologist, and perhaps others – and it may be impossible for the patient to find them all in-network at the same place. Sometimes the result is that EPO patients pay more going through their insurance company than if they pay cash – meaning their “insurance” is not really insurance.

Robert Book : A health economist and Senior Research Director at Health Systems Innovation Network LLC, a health policy research and consulting firm, and serve as a Health Care

While the debate proceeds over some details of the American Health Care Act, it’s worth pausing to take another look at how awfully misnamed the so-called “Affordable” Care Act has turned out to be, especially for people who buy their health plans on their own, rather than obtain it through an employer. While advocates and politicians have cited numerous examples of people facing huge premium increases, ACA advocates have been able to respond that those are cherry-picked cases, or that premiums were increasing before the ACA and would have increased anyway.

Those responses are no longer plausible. It turns out that across the board, for all ages and family sizes, for HMO, PPO, and POS plans, premium increases averaged about 60 percent from 2013, the last year before ACA reforms took effect, to 2017. In same length of time preceding that, all groups experienced premium increases of less than 10 percent, and most age groups actually experienced premium decreases, on average.